Frankly Speaking 9/7/21 - The Hype Rorschach Test

Hope everyone had a great summer! I decided not to write in August so that I can take a break and give others a break. Every month since March 2020 has been the busiest month of my career (including the busiest months of my PhD!). Anyway, I thought I would try something different for my first post back. Also, I am coming back from vacation :).

I had a conversation with David Zhou, and he turned our conversation into an awesome blog post. I’ve decided to have him be my first Let’s Be Frank guest post! You can also view his original blog post.

If you’re ever interested in collaborating on a post, send me a note! Conveniently, Substack is now allowing collaboration with guests, which I think is an awesome feature.

Onto the post!

LET’S BE FRANK (Guest Post)

Not too long ago, I quoted Phil Libin, founder of All Turtles and mmhmm (which has been my favorite virtual camera in and most likely post-pandemic), who said: “I think the most important job of a CEO is to isolate the rest of the company from fluctuations of the hype cycle because the hype cycle will destroy a company. It’ll shake it apart. In tech the hype cycles tend to be pretty intense.”

Hype is the difference in expectation and reality. Or more specifically, the disproportionate surplus of expectation. A month ago, Sarah Tavel at Benchmark wrote: “Hype — the moment, either organic or manufactured, when the perception of a startup’s significance expands ahead of the startup’s lived reality — is an inevitability. And yet, it’s hard not to view hype with a mix of both awe and fear. Hype applied at the right moment can make a startup, while the wrong moment can doom it.”

Right now, we are in a hype market. And hype has taken the venture market by storm.

We’ve all been seeing this massive and increasing velocity and magnitude of capital deployment over the last few months. Startups are getting valued more and more. In the past, the pre-money valuations I was seeing ranged from 2-on-8 to 3-on-9. Or in not so esoteric VC jargon, $2M rounds on $8M pre-money valuations ($10M post-money) to $3M rounds on $9M pre-money valuations ($12M post-money). These days, I’ve been seeing 5-on-20 or 6-on-30. Some of which are still pre-traction, or even pre-product.

Founders love it. They’re getting capital on a discount. They’re getting greater sums of money for the same dilution. Investors who invested early love it. Their paper returns are going through the roof. When looking at IRR or TVPI (total value to paid-in capital – net measurement on realized and unrealized value), higher valuations in their portfolio companies are giving investors jet fuel to raise future funds. And greater exit values on acquisition or IPO mean great paydays for early investors. Elizabeth Yin of Hustle Fund says “this incentivizes investors to throw cash at hyped up companies, instead of less buzzy startups that may be better run.”

Sarah further elaborated, “In the reality distortion field of hype, consumers lean in and invest in a platform with their time and engagement ahead of when they otherwise might have. They pursue status-seeking-work, not because they necessarily get the reward for it relative to other uses of their time, but because they expect to be rewarded for it in the future, either because of the typical rich-get-richer effect of networks, or just in the status of being an early adopter in something that ends up being big.” The same is true for investors investing in hyped startups. It’s status-seeking work.

Frankly, if you’re a founder, this is a good time to be fundraising.

Why?

Capital is increasingly digital.

There is more than one vehicle of early stage capital.

There are only two types of capital: Tactical capital and distribution capital.

1. Capital is increasingly digital.

Of the many things COVID did, the pandemic accelerated the timeline of the venture market. Pre-pandemic, when founders started fundraising, they’d book a week-long trip to the Bay Area to talk to investors sitting on Sand Hill Road. Most meetings that week would be intro meetings and coffee chats with a diverse cast of investors. Founders would then fly back to their home base and wait to hear back. And if they did, they would fly in once again. This process would inevitably repeat over and over, as the funnel grew tighter and tighter. And hopefully, at the end of a six-to-twelve month fundraise, they’d have one, maybe a few term sheets to choose from.

Over the past 18 months, every single investor took founder meetings over Zoom. And it caused many investors to realize that they can get deals done without ever having to meet founders in-person. Of course, the pandemic forced an overcorrection in investor habits. And now that we’re coming out of isolation, the future looks like: every intro meeting will now be over Zoom, but as founders get into the DD (due diligence) phases or in-depth conversations, then they’ll fly out to meet who they will marry.

It saves founders so much time, so they can focus on actually building and delivering their product to their customers. And,

VCs can meet many more founders than they previously thought possible.

This has enabled investors to invest across multiple geographies and build communities that breathe outside of their central hub or THE central hub – formerly the SF Bay Area. Rather, we’re seeing the growth of startup communities around the nation and around the world.

2. There is more than one vehicle for early stage capital.

While meetings have gone virtual, the past year has led to a proliferation of financing options in the market as well. Capital as jet fuel for your company is everywhere. Founders now have unprecedented optionality to fundraise on their terms. And that’s great!

Solo capitalists

Individual GPs who raise larger funds than angels and super angels, so that they can lead and price rounds. The best part is they make faster decisions that funds with multiple partners, which may require partner buy-in for investments.

Rolling funds

With their 506c general solicitation designation, emerging fund managers raise venture funds faster than ever and can start deploying capital sooner than traditional 506b funds.

Micro- and nano-VCs

Smaller venture funds with sub-ten million in fund size deploying strategic checks and often leverage deep GP expertise. No ownership targets, and can fill rounds fast after getting a lead investor.

Equity crowdfunding

Platforms, like Republic and SeedInvest, provide community-fueled capital to startups. Let your biggest fans and customers invest in the platform they want to see more of in the future. With recent regulations, you can also raise up to $5 million via non-accredited and accredited investors on these platforms.

Accelerators/incubators

Short three-month long programs, like Y Combinator, 500 Startups, and Techstars, that write small, fast checks (~$100K) to help you reach milestones. Little diligence and one to two interviews after the application. Often paired with an amazing investor and/or advisor network, workshops, powerful communities, and some, even opportunity funds to invest in your next round.

Syndicates/SPVs

Created for the purpose of making one investment into a company a syndicate lead loves, syndicates are another ad hoc way of raising capital from accredited investor fans, leveraging the brand of syndicate leads and deploying through SPVs. Or special purpose vehicles. I know… people in venture are really creative with their naming conventions. In turn, this increases discoverability and market awareness for your product.

SPACs and privates are going public again

Companies going public mean early employees have turned into overnight millionaires. In other words, accredited investors who are looking to grow their net worth further by investing in different asset classes. Because of the hype, investing in venture-scale businesses tend to be extremely lucrative. These investors also happen to have deep vertical expertise, high-value networks, as well as hiring networks to help startups grow faster. More investors, more early stage capital.

Growth and private equity are going upstream

Big players who usually sat downstream are moving earlier and earlier, raising or investing in venture funds and acceleration programs to capture venture returns. And as a function of such, LPs have increased percent distributions into the venture asset classes, just under different names.

Pipe

Pipe‘s existed before the pandemic, but founders have turned their eye towards different financing options, like Pipe. They turn your recurring revenue into upfront capital. Say a customer has an annual contract locked in with you, but is billed monthly. With Pipe, you can get all that promised revenue now to finance your startup’s growth, instead of having only bits and pieces of cash as your customers pay you monthly. Non-dilutive capital and low risk.

3. There are only two types of capital: Tactical capital and distribution capital.

There’s an increasingly barbell distribution in the market. Scott Kupor once told Mark Suster that: “The industry’s gonna bifurcate. You’re going to end up with the mega VCs. Let’s call them the Goldman Sachs of venture capital. Or the Blackrock of venture capital. And on the other end, you’re going to end up with niche. Little, small people who own some neighborhood whether it’s video, or payments, or physical security, cybersecurity, physical products, whatever. And people in the middle are going to get caught.”

Those “little, small” players have deep product and go-to-market expertise and networks. Their checks may be small. But for an early stage company still trying to figure out product-market fit, the resources, advice, and connections are invaluable to a startup’s growth. They’re often in the weeds with you. They check your blind side. And they genuinely empathize with the problems and frustrations you experience, having gone through them not too long ago themselves. Admittedly, many happen to be former or active operators and/or entrepreneurs.

On the flip side, you have the a16z’s and Sequoias on their 15th or 20th fund. Tried and true. Brilliant track record with funds consistently north of 25% IRR. Internal rate of return, or how fast their cash is appreciating annually. LPs love them because they know these funds are going to make them money. And as any investor knows, double down on your winners. More money for the same multiples means bigger returns.

The same is true for historical players, like Tiger, Coatue, and Insight, who wire you cash to scale. They assume far less risk. Which admittedly means a smaller multiple. And to compensate for a lower multiple, they invest large injections of capital. By the time you hit scale, you already know what strategies work. All you need is just more money in your winning strategies.

You find product-market fit with tactical capital. You find scale with distribution capital.

Product-market fit is the process of finding hype. When you stop pushing and start finding the pull in the market. Scale is the process of manufacturing hype.

The bear case

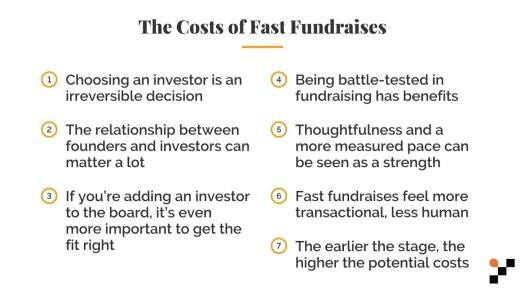

But there are downsides to hype. Last month, Nikhil, founding partner at Footwork, put it better than I ever could.

If I could add an 8th point to Nikhil’s analysis, it’d be that investors in today’s market are incentivized to “pump and dump” their investments. Early stage investors spike up the valuations, which leads to downstream investors like Tiger Global, Coatue, Insight, and Softbank doubling down on valuation bets. Once there’s a secondary market for private shares, early stage investors then liquidate their equity to growth investors who are seeking ownership targets, or just to get a slice of the pie. This creates an ecosystem of misaligned incentives, where early stage investors are no longer in it for the long run with founders. Great fund strategy that’ll make LPs happy campers, but it leaves founders with uncommitted, temporary partners.

Sundeep Peechu of Felicis Ventures has an amazing thread on how getting the right founder-investor fit right is a huge value add. And getting founder-investor fit takes time, and sometimes a trial by fire as well. After all, it’s a long-term marriage, rather than a one-night stand. Those who don’t spend enough time “dating” before “marriage” may find a rocky road ahead when things go south.

On a 9th point, underrepresented and underestimated founders are often swept under the rug. In a hype market, VCs are forced to make faster decisions, partly due to FOMO. With faster decisions, investors do less diligence before investing. Which to the earlier point of misaligned incentives, has amplified the already-existing notion of buyer’s remorse.

When VCs go back to habits of pattern recognition, they optimize for founder/startup traits they are already familiar with. And often times, their investment track record don’t include underrepresented populations. To play devil’s advocate, the good news is that there is also a simultaneous, but comparatively slow proliferation of diverse fund managers, who are more likely to take a deeper look at the problems that underestimated founders are tackling.

What kind of curve are we on?

When many others seem to think that this hype market will end soon, last week, I heard a very interesting take on the current venture market in a chat with Frank Wang, investor at Dell Technologies Capital. “VCs have been mispricing companies. We anchor ourselves on historical valuations. But these anchors could be wrong.

“We’re at the beginning of the hype and I don’t see it slowing down. VC has been so stagnant, and there hasn’t been any innovation in venture in a long time. Growth hasn’t slowed. And Tiger [Global] and Insight [Partners] is doing venture right. Hypothetically speaking, if you invest in everything, the IRR should be zero. They are returning 20% IRR because they seem to have found that VC rounds are mispriced. So, there can be an arbitrage.

“There will be a 20% market correction in the future, but we don’t know if that’s going to happen after 100% growth, or correct then grow again. The current hype is just another set of growing pains.”

Part of me is scared for the market correction. When many founders will be forced to raise flat or down rounds. The fact is we haven’t had a serious market correction since 2009. It’s going to happen. It’s not a question of “if” but rather “when” and “how much”, as Frank acutely points out.

Investors who deploy capital fast win on growing markets – on bull markets. Or investors who deploy across several years, or what the afore-mentioned Mark Suster defines as having “time diversity“, who win on correcting markets – bear markets. Think of the former as putting all your eggs in one basket. And if it’s the winning basket, you’re seen as an oracle. If not, well, you disappear into obscurity. Think of the latter as diversifying your risk appetite – a hedging strategy. More specifically, (1) being able to dollar-cost average, and (2) having exposure to multiple emerging trends and platforms. You’re not gonna lose massive amounts of capital even in a bear market, but you also will be losing out on the outsized returns on a bull market.

Only time will tell how seriously the market will correct and when. As well as who the “oracles” are.

In closing

At the end of the day, there are really smart capital allocators arguing for both sides of the hype market. Like with all progress, the windshield is often cloudier and more muddled than the rearview mirror. As Tim Urban once wrote, “You have to remember something about what it’s like to stand on a time graph: you can’t see what’s to your right.“

And as founders are going to some great term sheets from amazing investors, I love the way Ashmeet Sidana of Engineering Capital frames it earlier this year. “A company’s success makes a VC’s reputation; a VC’s success does not make a company’s reputation. In other words to take a concrete example, Google is a great company. Google is not a great company because Sequoia invested in them. Sequoia is a great venture firm because they invested in Google.”

Whether you, the founder, can live up to the hype or not depends on your ability to find distribution before your competitors do and before your incumbents find innovation. Unfortunately, great investors might help you get there with capital, but having them on your cap table doesn’t guarantee success.

Nevertheless, the interpretation of hype is always an interesting one. There will continue to be debates if a market, product, or trend is overhyped or underhyped. The former assumes that we are on track for a near-term logarithmic curve. The latter assumes an immediate future looking like an exponential curve. The interpretation is, in many ways, a Rorschach test of our perception of the future.

Over the course of human civilization, rather than an absolutely smooth distribution, we live something closer to what Tim Urban describes as:

If the regression line is the mean, then we’d see the ebbs and flows of hype looking something like a sinusoidal function. As Mark Twain once said, “History doesn’t repeat itself, but it often rhymes.”

It won’t be a smooth ride. The world never is. But that’s what makes the now worth living through.